Global PVC prices have been on a downward trajectory since around mid-April, while sentiment has recently turned more bearish particularly in Asia under the light of recent developments.

Among the prominent factors signaling further downfall in prices are weaker commodity demand – ruffled by rampant inflation, rising supplies in major markets, fresh Covid-19 fears in China amid its already brittle economy, the monsoon season in India, and the plunge in energy futures.

Chinese suppliers’ aggressive approach in export outlets including India, Southeast Asia, Turkey and Egypt has already triggered a price competition among main suppliers of PVC. On top of the existing pressure from China , some very aggressive PVC K67 offers from the US have emerged in Asia this week, raising the question of whether the markets are poised to take a deeper dive in the near term.

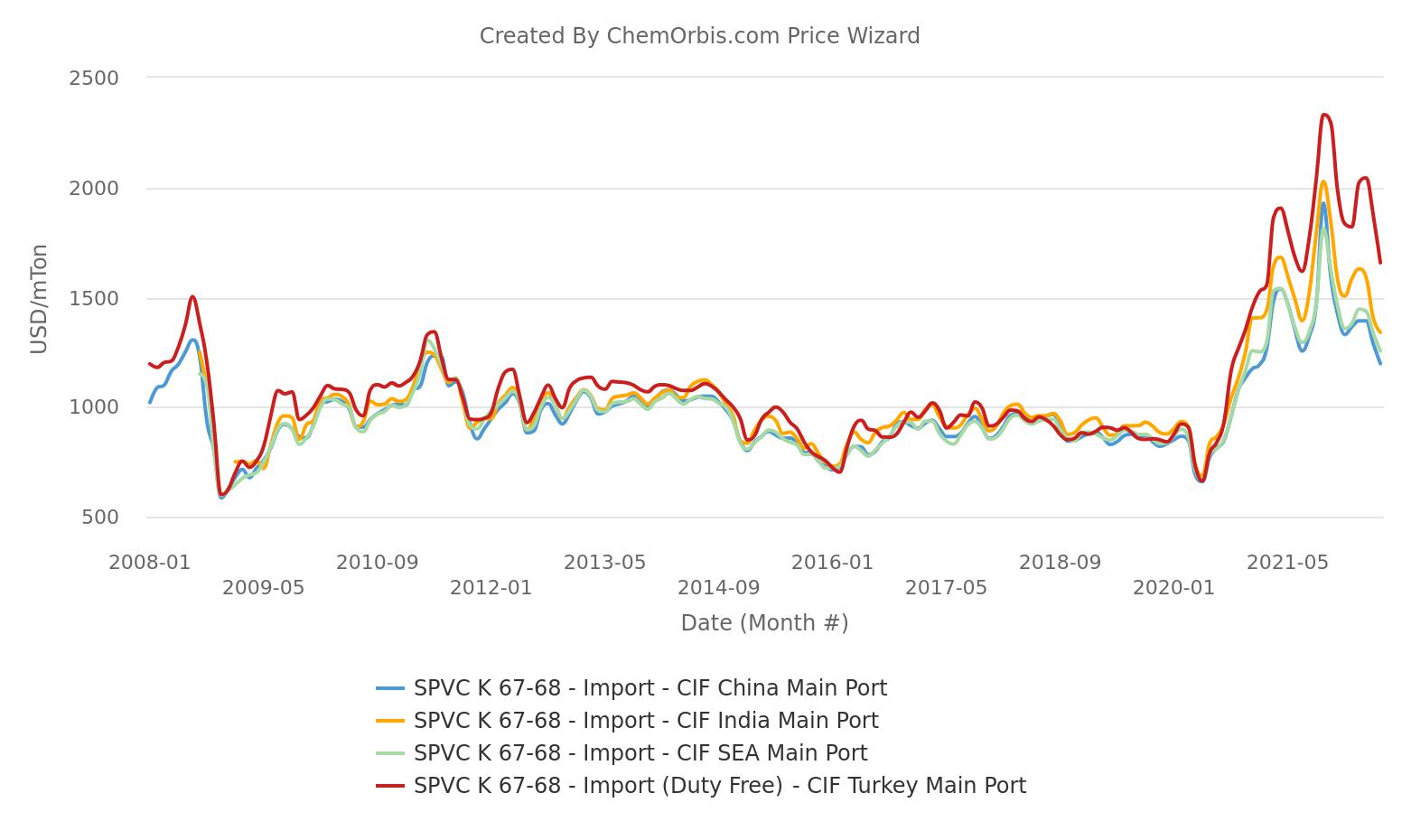

Prices are down from record highs, but still much above pre-pandemic levels

Will PVC see its pre-pandemic levels ever again? This was the big question in players’ minds when prices hit unprecedented highs in October 2021. Compared to that point, import K67 prices in major markets including India, China, Southeast Asia, and Turkey have lost around 30-40%.

However, there is still a long way for PVC to go back to its pre-pandemic levels, as data show.

ChemOrbis Price Index suggests that the current weekly averages of import K67 prices are standing $350/ton above pre-pandemic levels in India, $265/ton in China, $295/ton in Southeast Asia, and $610/ton in Turkey.

Not China, this time. Plunging US offers take the lead in a nosedive in Asia

On June 21, the major Taiwanese producer announced its July offers to Asia with a $90/ton decrease at $1120/ton CIF China and at $1320/ton CIF India. Following the producer’s price notifications, much lower offers for different origins popped up in the markets.

A few traders in India said that they received competitive Chinese acetylene-based K67 offers at $1200s/ton CFR right after the Taiwanese major’s July announcement. “The Indian market is well supplied amid the continuing flow of competitively-priced Chinese PVC,” they noted.

As the week progressed, even more aggressive offers started to emerge from the US, probably offered from the short-positions of traders. Players reported that US K67 was offered at $1050/ton CIF China and at $1020-1080/ton CIF Vietnam.

A Vietnamese converter said, “US K67 with August delivery has been offered at $1020/ton CIF this week and we heard that a deal was closed for 1000 tons at this level, which is quite competitive.”

Turkey also sees sharper than expected drops in June

Apart from persistently weak demand, there has been a slew of factors paving the way for sharper than anticipated June drops in Turkey. Supplies were palpable, with an influx of import cargoes for various origins exacerbating sales pressure.

Russian PVC cargoes have been a major pressure point since they boosted their market share in Turkey, dethroning Europe and becoming the top PVC supplier in the first four months of 2022. Russian K67-68 with 6.5% customs duty broke below the $1450/ton CIF level late last week, while stocks at warehouses were reported to be plentiful.

Amid stiff competition with the influx of Russian PVC, other origins mainly China, South Korea, Egypt and the US lowered their prices one after another in Turkey in the past couple of months. Even import prices from Europe, where buyers have scrambled to find cargoes, were down by at least 20% in the past three months.

Signs of improved supplies from Europe

It has been almost two years since Turkish buyers received less and less PVC supply from European suppliers due to long-lasting production snarls across the region.

Given the record-high premium Europe carries over the rest of the world and the expected decrease in the next monomer contract, some market players in Turkey opine that European suppliers will be more willing to focus on exports to their main outlet in July, particularly when the slump is set to gain momentum in the rest of the world.

(Source: chemorbis)