January PE prices emerged with rollovers to monthly drops in Europe. Although the delayed arrival of US cargoes supported regional suppliers to some extent, growing supplies amid better import availability and tepid demand put pressure on particularly LDPE and HDPE grades.

Offers from nearby sources see discounts

Although prices for European origins have been mostly rolled over, non-European PE origins emerged with monthly drops as sellers yielded to the muted demand and improving supply levels. Weak dynamics and the emergence of more competitive offers from nearby countries put pressure on regional producers.

Supplies grow despite production disruptions

In Europe, maintenance shutdowns or other production hiccups have had no visible impact so far. Several players attributed this to the fact that producers have built safety stocks ahead of their turnarounds. Plus, stocks are higher as distributors and converters purchased beyond their needs in the previous months to minimize logistics disruptions.

In production news, Versalis shut its LDPE plant in Ragusa, Italy for a planned maintenance from January 10 to February 28, while Dow declared a force majeure on PE output following the shutdown of its cracker in Terneuzen, the Netherlands.

Buying fatigue kicks in after relentless hikes

Earlier replenishment activities and lingering holiday lull kept demand subdued in January. Apart from that, PE buyers in Europe have been overwhelmed with steep hikes in raw material prices and surging energy costs.

Rising energy costs are likely to deal a fresh blow to downstream companies, who would prefer to run at lower rates to alleviate cost burden. This may even boost exports of end products to Europe in the longer run, a few players argued.

US PE moves below European origins

Contrary to the past few months, import US PE offers currently offer a competitive edge against European origins. US prices stood slightly below the spot ranges in Italy at €1730-1750/ton DDP, 60 days for LDPE film. US HDPE film with delivery in March was offered at €1500/ton, meanwhile.

Omicron appears to be becoming the dominant variant across the board, which adds to the logistics disruptions amid trucker shortage, reduced manpower and slower port operations. Ongoing logistics backlogs curbed the import flow from the US and the arrival of these cargoes has been delayed many times. Although logistics challenges are here to stay, more US PE cargoes are awaited to hit European shores in February.

Europe preserves its charm for importers

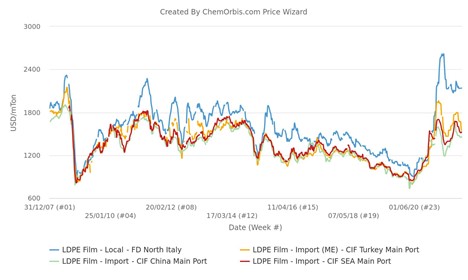

With Europe offering the most attractive netback, it is too obvious that importers will be motivated to sell to this market. Spot LDPE prices both in Italy and West Europe still stand at an all-time high even though they came off their peaks months ago, ChemOrbis Price Index revealed.

PE prices across Europe carry a huge premium over other global markets as regional markets remained isolated due to the logistical hurdles.

As can be seen on the graph below, LDPE film prices in Italy’s local market trade at a large premium over other markets. Import LDPE prices reported in China, SEA and Turkey are on CIF, cash terms, not including any customs clearance and inland transportation costs.

Italy traditionally carries a premium over other these markets as its local LDPE prices are for prompt cargoes including all duties if applicable and delivery cost to buyers’ plants.

February calls for drops

Participants suggested that January PE deals will be mostly closed with monthly decreases, considering comfortable stocks both on the sellers and buyers’ side. Some sellers in the distribution channel are keen to reduce their stocks. The emergence of more competitive offers for non-European origins and the expected arrival of import cargoes keep the February outlook weak.

LLDPE C4 film likely to remain resilient as short mLL C6 spurs demand

Unlike LDPE and HDPE, LLDPE C4 film prices are not believed to be under a visible downward pressure due to the increased demand from mLLDPE C6 buyers. Tightness forced buyers to switch to LLDPE C4 film, which may prop up prices.

(Source: ChemOrbis)