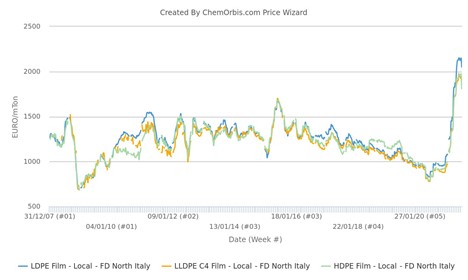

Europe’s PE markets have reversed the course after seven straight months of hikes to recede from their all-time highs on the back of aggressive import offers and growing resistance against inflated prices.

PE suppliers initially approached the market with rollovers to increases for European origins, with the support from the ethylene hike. However, they had to take a step back and apply discounts in a bid to stimulate buying interest as the month wore on.

Non-European origins stand well below spot ranges

Aggressive imports have served to cease the 7-month bullish rally in the spot market. Europe’s massive premium over other global markets attracted more import cargoes. Arriving imports brought some relief to the regional markets, which had been grappling with tightness amid production glitches and logistical hurdles impeding imports.

Non-European origins stand roughly €200-300/ton below the prevailing spot ranges, which adds to the pressure on the regional suppliers.

As for LDPE, Saudi material was offered at €1950/ton FD Italy, 60 days. Although not widely confirmed at the time of writing, a few buyers reported offers at or slightly below the €1900/ton FD level. Russian, Saudi, and US LLDPE C4 film was offered within the range of €1600-1650/ton with the same terms.

HDPE film offers stood at €1480-1500/ton for various origins, while Egyptian HD b/m was offered at €1420/ton. In Germany, US and Egyptian HDPE inj. deals stood at €1600-1650/ton FD, 60 days.

PE still at record-highs after drops

Spot PE markets on FD Italy/NWE basis still stand at all-time highs after coming off their peaks. Meanwhile, the pressure on LDPE was rather moderate compared to other grades. HDPE grades saw sharper decreases.

Despite the recent fall, the weekly average of LDPE and LLDPE prices on FD Italy basis remained 113% higher than the levels in November 2020, when the uptrend first kicked off. HDPE grades still stand nearly 90-100% above November levels, meanwhile.

Decrease expectations put buyers off

June drops failed to stir demand as buyers expect spot prices to retreat further in the latter half of the month and July. They refrain from committing to new materials, considering the fact that prices still stand at inflated levels. A converter said, “End customers have also been sidelined as they wait to see raw material decreases, which is crimping activity in general.”

On the evening of June 5, the launching ceremony of the national COVID-19 vaccine fund in Hanoi was held with the presence of the Prime Minister, representatives of leaders of government, enterprises and organizations.

Deputy Prime Minister Le Minh Khai (right) presented donation certificate to Mr. Pham Van Tuan – Acting Deputy CEO of An Phat Holdings (left)

Attending the event, An Phat Holdings was honored to receive the Government’s commendation as pioneer donor to the national COVID-19 vaccine fund. Representative of An Phat Holdings’ management, Mr. Pham Van Tuan – Acting Deputy CEO of the Group received certification for making contribution of VND 20 billion (~$ 851,000) to the national COVID-19 vaccine fund.

In the fight agaisnt COVID-19, An Phat Holdings wishes to contribute to the community, demonstrating the social responsibility of businesses for the country to quickly stamp out Covid-19.

See more pictures at the event:

An Phat Holdings attended the event as a typical enterprise making contribution to the national Covid-19 vaccine fundRepresentative of managements of An Phat Holdings, Mr. Pham Van Tuan – Acting Deputy CEO of the Group (left) received certification of donating VND 20 billion (~$ 851,000)

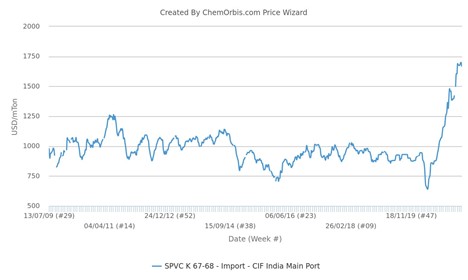

The blockbuster rally in India’s PVC market has run out of steam and import K67 prices have receded from their all-time highs this week in the face of rapidly reduced demand amid a second wave of deadly infections.

Import PVC K67 prices of overall origins were assessed $30/ton lower from last week at $1640-1700/ton CIF India, cash basis.

Despite the fall, the weekly average of PVC prices on CIF India basis remained 260% higher than the levels in May 2020, when the longest ever price rally first kicked off.

Import PVC prices CIF India

COVID-19 crisis likely to dampen pre-monsoon buying interest

India’s death toll from the pandemic has gone beyond 200,000 amid a shortage of oxygen, medical supplies and hospital staff. The deadly second wave has seen around 300,000 people tested positive for the virus daily which has overwhelmed healthcare facilities.

PVC players in the country reported that downstream manufacturing sectors are again facing disruptions since more states impose fresh curbs on public movement and transport to contain the spread of the virus. “We might face closures at ports due to partial lockdowns, and PVC supplies to the country might be disrupted,” a few players commented.

With the surge in COVID-19 cases yet to reach its peak, market players expect sharp pressure on PVC demand and prices in the near term. “We may not see the traditional demand increase ahead of the monsoon season this year due to the COVID crisis in the country,” noted traders.

India’s monsoon season lasts from June to September and stretches longer in some years. During that period, heavy rains impede both building construction and agriculture sectors while rough seas make loading and unloading at ports difficult.

Prices may remain under pressure despite still-tight supplies

Most players believe that PVC prices in India may remain under pressure over the near term given fading demand amid the second wave of the pandemic.

“We might see lower June offers from a major Taiwanese producer despite the ongoing shortage of availability across regional and global markets,” some commented.

The Taiwanese major lifted its May offers by $30/ton after applying a massive hike of $300/ton for April.

Plastics processors are increasingly alarmed by what is in many places a short supply of granulate (Photo: PantherMedia/kriengst@scg.com)

“We want to avoid a second 2015,” says Ron Marsh, chairman of the Polymers for Europe Alliance (www.polymercomplyeurope.eu/pce-services/polymers-europe-alliance), an initiative in association with EuPC (Brussels / Belgium; www.plasticsconverters.eu). There has been an alarming increase in forces majeures, says Marsh, especially towards the end of 2020. PVC is affected, but recent weeks also saw an increasing scarcity of LDPE, ABS, isocyanates and polyols in some cases, and in many cases considerably higher prices, as Plasteurope.com reported.

According to PIE’s Polyglobe database (www.polyglobe.net), the number of European FM cases in 2020 is average compared to previous years. A concentration can, however, be noted towards the end of the year.

Apparently, the alliance, which was founded in 2015 due to a dramatic shortage of materials on European markets at that time (see Plasteurope.com of 02.07.2015), does not consider the situation to be quite as precarious as in its founding year – though the atmosphere between producers’ organisation PlasticsEurope (Brussels; www.plasticseurope.org) and the EuPC is anything but relaxed, as usual. Nevertheless, EuPC is not the only association sending out alarm signals.

French national plastics and composites converters association Fédération de la Plasturgie et des Composites (FEP, Paris), which is now part of the umbrella organisation for French plastics processors Polyvia (www.polyvia.fr), founded on 31 December 2020, has voiced similar concerns. The association addresses the “rapid price increases” and “increasing risk of production interruptions.” Under the leadership of Emmanuelle Perdrix, president of French injection moulder Rovip (Nivigne et Suran; www.rovip.com), and Jean Martin, former director general at FEP and now Polyvia’s general manager, the federation warns producers not to take advantage of the situation and “impose contracts without any possibility of negotiation.” The explanations offered by the producers for the shortfalls, says Martin, are “insufficient for the current situation.” Both federations – EuPC and Polyvia – signalled their willingness to communicate with producers, emphasising the “urgent need for talks in order to not damage the climate of mutual trust.” To elaborate, Polyvia says it is working to find solutions to the “totally unbalanced situation” of forces majeures either not corresponding to fittingly major situations, or clients of plastics manufacturers not taking these situations seriously into account.

The situation in Germany is more relaxed, and Martin Engelmann of Industrievereinigung Kunststoffverpackungen (IK, Bad Homburg / Germany; www.kunststoffverpackungen.de) reported widespread calm from the packaging sector. However, Michael Weigelt, managing director of TecPart (Frankfurt / Germany; www.tecpart.de) responsible for statistical issues in the Gesamtverband Kunststoffverarbeitende Industrie (GKV, Berlin / Germany; www.gkv.de), confirms that there are strong price movements for engineering thermoplastics.

“We have been observing the situation since December,” he said. “Asia is paying higher prices, and there is also a lack of imports from the US and Middle East, some of which is also flowing to Asia,” Weigelt told PIE. Long-term customer contracts should still be reliably supplied, but companies increasing production on short notice, thus requiring more material, will have to be prepared for long delivery times. On the other hand, he does not see any actual raw material bottlenecks – although PA 6.6 is likely to be an exception at this point. The feedstock chain for the polyamide grade seems to be quite tight after a few outages.

In Africa, regional markets kicked off February on a strong note as a continued tightness in supplies kept sellers’ stance bullish. However, demand was moderate-to-weak across the continent as COVID-19 related concerns remained as the key driver.

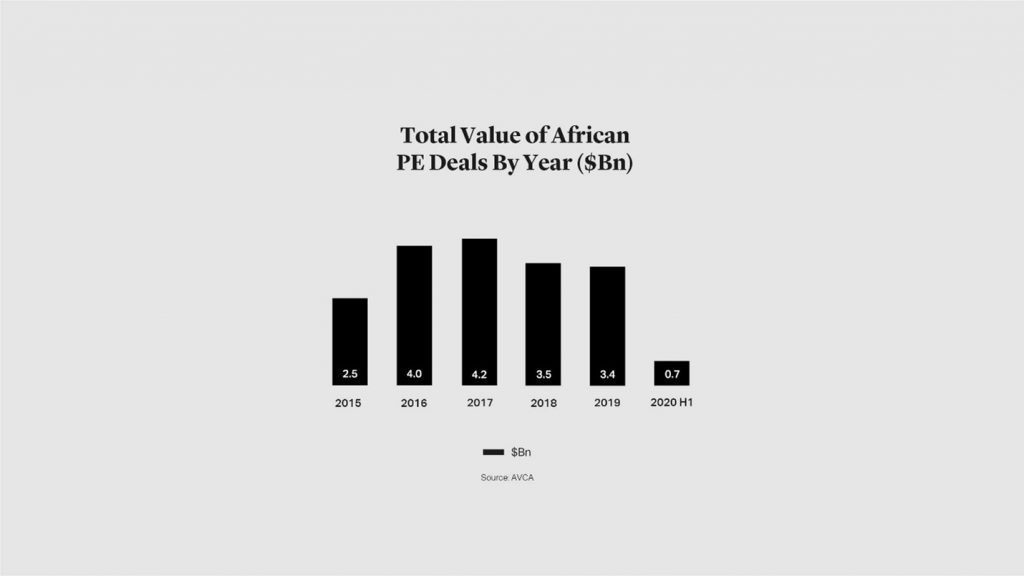

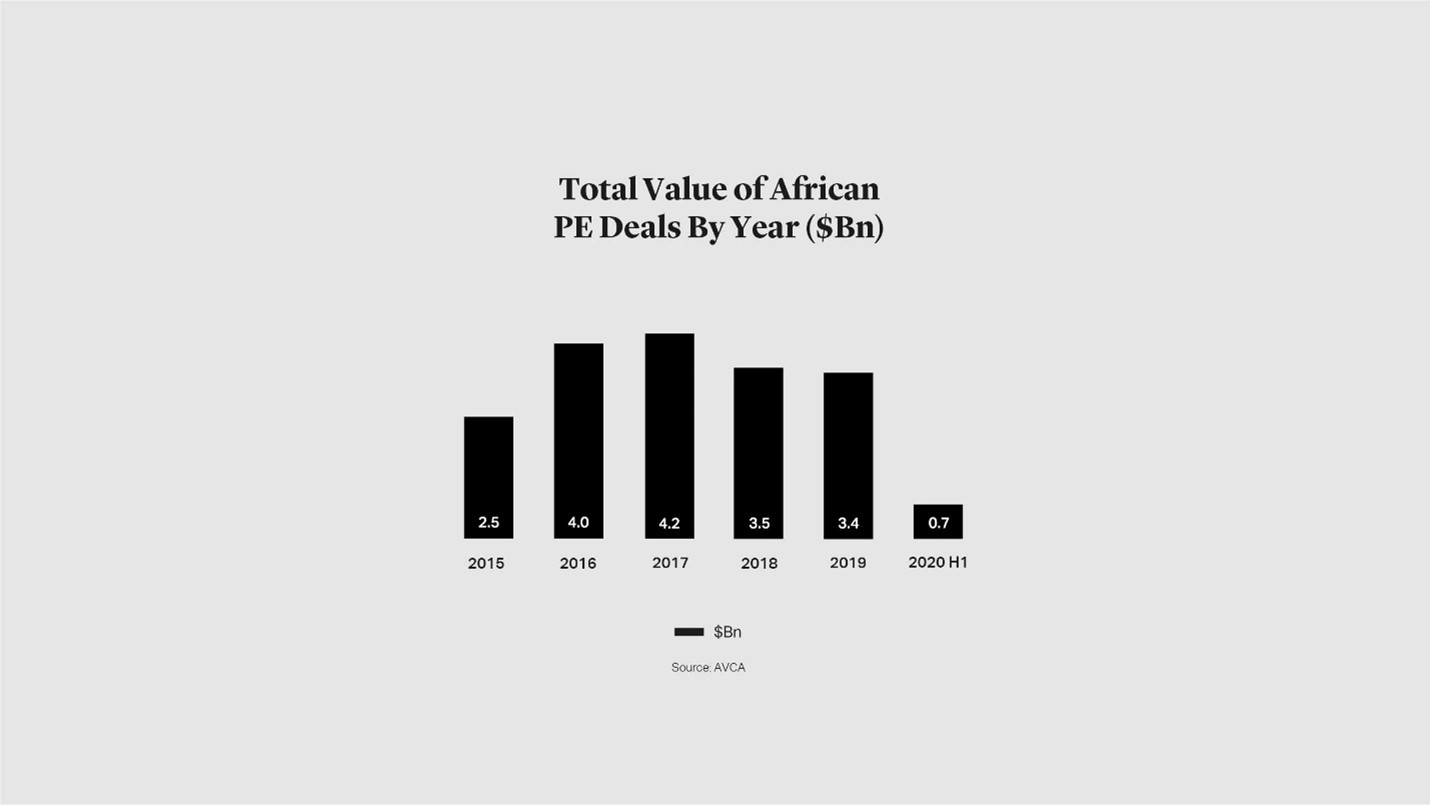

Total value of African PE Deals By year ($Bn)

Nigerian producer ops for hikes amid tight allocations

In Nigeria, a key market for polymers in Africa, February offers from a domestic producer were higher over January levels. Accordingly, the local producer ELEME announced increases of NGN40,000/ton ($105/ton) for PE grades and also increases of NGN110,000/ton ($289/ton) for PP grades.

These changes brought the producer’s February price list to NGN836,800/ton ($2199/ton) for PPH raffia and inj., NGN863,000-867,500/ton ($2268-2280/ton) for PPBC inj., NGN7800,000/ton ($2102/ton) for HDPE b/m, HDPE film, and HDPE inj., and NGN757,000/ton ($1989/ton) for LLDPE C4 film, all on ex-Port Harcourt City, cash not including 7.5% VAT.

“Market players are still waiting to hear more offers from the Middle Eastern before committing to any fresh purchases,” a converter said, adding that the local producer’s allocations were quite limited. ELEME was heard to be running at lower operating rates but this was not confirmed directly by the producer.

LDPE, PPH raffia-inj. prices at highest since 2015 in Kenya

New import PP and PE prices in Kenya, the largest economy in East Africa, remained on an upward trajectory in February. Saudi HDPE film and LDPE film grades saw monthly increases of $60-70/ton and $80-90/ton respectively while LLDPE C4 film offers increased by $100/ton over January. Offers for Saudi and Chinese PPH raffia and inj. materials were also higher by $90-100/ton from last month.

Accordingly, the latest prices in Kenya were at $1230-1250/ton for HDPE film and HDPE inj., $1280-1300/ton for HDPE b/m, $1200-1220/ton for LLDPE C4 film, $1520-1550/ton for LDPE film, $1420-1440/ton for PPH raffia, $1430-1440/ton for PPH inj., all on CFR Mombasa, Kenya, 90 days basis.

As ChemOrbis Price Index shows, these changes brought the weekly average of LDPE film and PPH raffia and inj. import prices to their highest since mid-2015. HDPE film and LLDPE film offers, meanwhile, stood at their highest in two and a half years.

“Supply remains very tight and some sellers refrained from offers this month. Demand is moderate but is a bit better than last month. COVID-19 situation is still worrying and the nightly curfew is in effect up to March 12,” a trader in Nairobi said.

Tightness brings hikes of up to $100/ton in Algeria

In Algeria, a key market in North Africa, LDPE film and HDPE film offers from a major Saudi supplier were $20-40/ton higher while LLDPE C4 film prices remained unchanged on a monthly basis. Saudi PPH raffia and inj. offers, meanwhile, increased by $70-100/ton from January.

The latest offers were at $1250/ton for HDPE film, HDPE inj., and LLDPE C4 film, $1500-1520/ton for LDPE film, $1420-1450/ton for PPH raffia and PPH inj., $1460-1470/ton for PPH film and PPH fibre, and $1580/ton for PPBC inj., all on CFR Algeria, 90 days basis.

“The availability for PPH, HDPE film and LLDPE C4 film is extremely tight. Demand is moderate and short availability has become a concern for market players as most of them are not able to source enough materials to operate their plants,” a trader in Algiers said.

Supply in balance as demand remains weak in S. Africa

In South Africa, February PE offers from the major Saudi supplier were $70-80/ton higher for HDPE film and LLDPE film, and also by $90-100/ton for LDPE film. The latest offers were at $1250-1280/ton for HDPE film, $1530-1560/ton for LDPE film and $1210-1230/ton for LLDPE C4 film, all on CIF, cash basis.

“Supply remains restricted but it is somehow balanced with demand. We think a market saturation point is near and sellers might not be able to push for higher prices next month,” a trader based in Durban said. As ChemOrbis Price Index shows, the monthly average of import PE prices in South Africa has risen by around 60% to 80% since mid-2020.

Today (25 Feb 2021) at the headquarters of the Vietnam Fatherland Front Committee of Hai Duong, the representative of the Board of Directors of An Phat Holdings (APH) handed over VND 20 billion (~ $851,000) support to the provincial government to buy vaccines for residents of Hai Duong in the fight against Covid-19. Previously, in 2 times of support on February 1 and February 17, APH donated VND 11.35 billion (~$482,000), including cash, necessities, and equipment … to the Hai Duong provincial government.

Thus, only in February 2021, the total value of VND 31.35 billion (~ $1,3 mil) was donated by APH in Hai Duong’s Covid-19 fight. Together with 3 times of support with cash and necessities, An Phat Holdings in coordination with Hai Duong’s Youth Union, individuals, organizations, businesses… launched campaign “Relief and rescue agricultural products of Hai Duong”, rescued 1,000 tons of farm products.

Hai Duong Province’s Leader received VND 20 billion (~$851,000) from the representative of An Phat Holdings, Mr. Pham Van Tuan – Acting Deputy CEO.

Present at the headquarters of the Vietnam Fatherland Front Committee of Hai Duong province, the representative of the Board of Directors of An Phat Holdings, Mr. Pham Van Tuan – Acting Deputy CEO of the Group directly handed over VND 20 billion (~$ 851,000) to Hai Duong’s government representative to support the implementation of buying Covid-19 vaccine for the resident of Hai Duong. Hai Duong Province’s Leaders directly received support from APH and expressed appreciation to the Board of Directors and An Phat Holdings’ employees.

This is also the biggest donation that An Phat Holdings has donated to the representatives of Hai Duong Province in Covid-19 pandemic prevention. Mr Pham Van Tuan – An Phat Holdings’ Acting Deputy CEO shared “In the situation of urgent need to have vaccines, helping people feel secure and helping the government to control the pandemic early is not only the responsibility of An Phat Holdings but also other organizations and individuals who want to contribute. All the support of An Phat Holdings from human or material resources comes from the spirit of unanimity, joining hands toward Hai Duong, hoping the province will quickly overcome the pandemic.”

Hai Duong Province’s Leader expressed appreciation for An Phat Holdings’ support

Hai Duong is the key production area of An Phat Holdings with 10 plants, many subsidiaries and is where 3,500 employees are living and working. Therefore, the Board of Directors and more than 5,000 employees of the whole Group are always ready to accompany and share all difficulties of Hai Duong in any period and at any time.

Along with the community support, An Phat Holdings always strictly complies with preventive measures at all factories, production facilities and offices, perform Covid-19 tests on all employees for ensuring “Safety for Employees, Safety for Production”.

Previously, in early 2020, since the outbreak of Covid-19 in Hanoi, An Phat Holdings also donated compostable products to 300 residents and soldiers on quarantine duty in Truc Bach area (Hanoi) and donated 5,000 medical masks and hand sanitizers to Vietnam Embassy in the United States.

2020 is not ending as many expected in the European polyethylene (PE) and polypropylene (PP) markets, and sentiment has changed significantly in the last few weeks.

2020 was expected to be a poor year, as imports of ethane-based PE, mainly from the USA, were expected to arrive in greater supply.

In fact, there was an increase in PE and PP packaging, caused by strong buying as the first wave of the coronavirus pandemic sent buyers rushing to the shops.

Other industries were shut down, such as automotive, where 10-11% of PP is used.

By the second half of the year most applications were returning to normal. Automotive has fared better than expected, and packaging is back to normal levels. Those involved in health and hygiene have remained good throughout.

The appliances sector also has recovered beyond expectations in H2 2020, including both small and large appliances.

By the end of the year, a slowdown in polyolefin buying is the norm, with the odd special deal thrown in to boost sellers’ volumes, but this has not been the case in 2020.

Low prices in Europe, both for PE and PP, have meant that exports became a strong feature of the fourth quarter of 2020, leading to a tight market, particularly in the PP sector. Hurricane Laura prevented US imports, which added to the tightness, generating export opportunities to Latin America, among other destinations.

Rather than December being a slow month peppered by offers of cut-price material, prices of both PE and PP have jumped, particularly for low density polyethylene (LDPE) and PP.

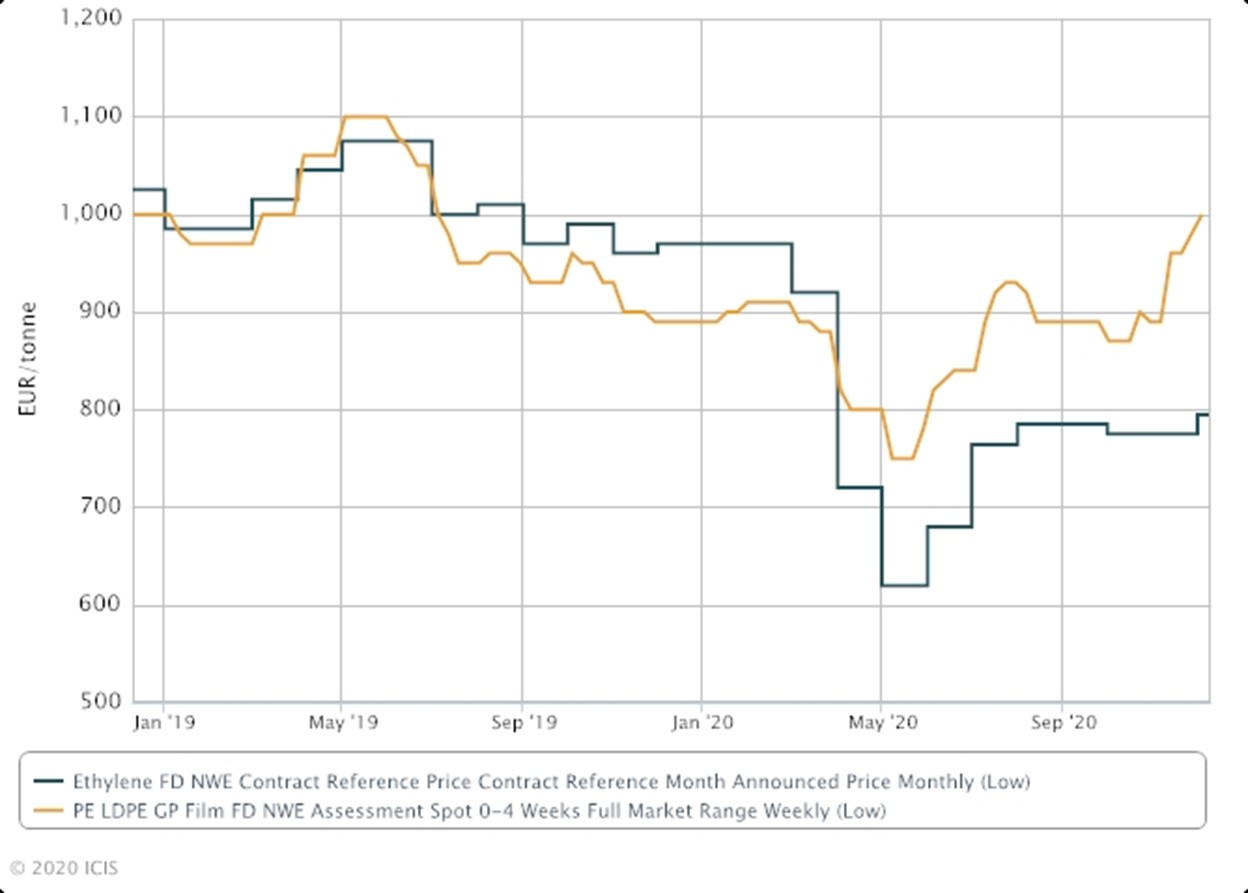

The spread between the ethylene contract and PE has widened in 2020, from a very low base in 2019.

Not only are prices rising amid tight supply, but some producers are already warning buyers that the upward trend could well continue into January.

The recent price hikes in Europe are shortening the gap with Asian prices after months of European stagnation, while corresponding prices in China were driven by stellar domestic demand, especially since mid-Q3 2020.

Buyers argue that December and January are short months. There may yet be time for some of the production issues contributing to the tightness to go back to normal, easing the short supply.

Imports are not expected to resume until well into the first quarter, according to many sources, however, and this will affect the market.

When fresh imports are expected to reach Europe, from late January 2021, domestic demand in China will decelerate ahead of the Lunar New Year holiday period. This will probably help to realign prices in the regions, according to ICIS analytics.

Annual contracts for 2021 are under discussion at this time of year, and while the current tightness favours sellers, the second half of 2021 is not expected to remain as strong, so some pragmatism is entering the debate. Contracts are by no means all done, but several buyers said they have managed to achieve discounts of a couple of percentage points over 2020 for PP.

PE is expected to be more readily available, as global supply increases.

In terms of PE demand, ICIS analytics expects a slow but constant recovery during 2021, accompanied by expectations of improved economic conditions in Europe and globally. However, the PE market in 2021 could face a strong supply increase as effective PE capacity globally is expected to increase by 6.5% in 2021 versus 2020. This is likely to lengthen the 2021 supply and demand balance.

Effective global high density polyethylene (HDPE) capacity, in particular, is expected to increase by more than 8% year on year in 2021, while global linear low density polyethylene (LLDPE) and LDPE capacities are expected to increase by 7% and 3% respectively, in the same period.

PP supply will increase considerably in 2021 and especially in Asia, where 7.7m tonnes/year of new capacity will be brought onstream, corresponding to 10% of the PP volume processed globally in 2020. The effect on pricing is expected to be felt on the markets especially in the second half of the year.

The global ethylene market should show signs of improvement throughout 2021, according to ICIS analytics, on the assumption that the worst of the coronavirus pandemic impact will be over. Uncertainty over economic growth and distribution of coronavirus vaccines, as well as their effectiveness, might significantly weigh on supply and demand fundamentals. European ethylene is expected to remain long as supply increases.

Globally, propylene demand should increase at a higher average annual growth rate than GDP in 2021, but much depends on how global economies fare.

PP supply will also increase and no tightness is expected, although PP is not expected to see the same oversupply as PE.

Ultimately demand in Asia, and more particularly China, will have a significant impact on both PE and PP trends in Europe in 2021.

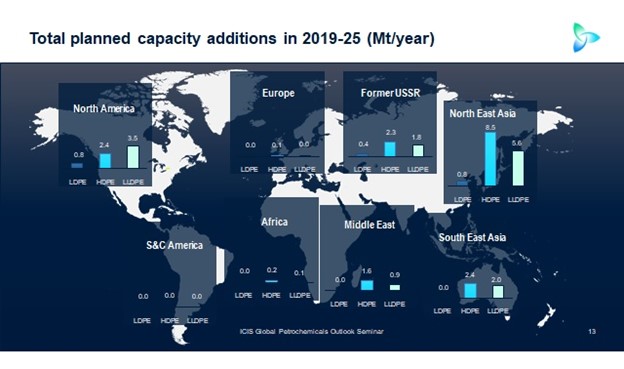

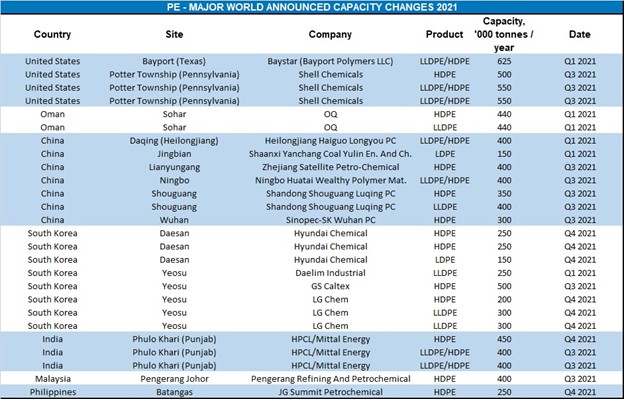

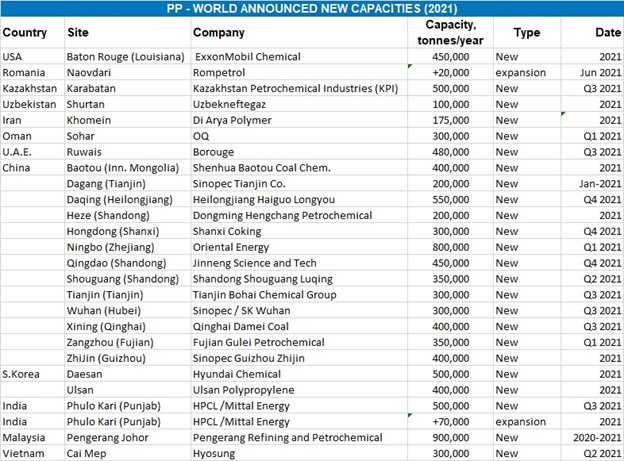

Total planned capacity additions in 2019 – 25PP capacity additions exceed demand growth in the short-termPE – Major world announced capacity changes 2021PP – World Annouced New Capacities (2021)

On February 17, 2021, at the headquarters of the Vietnam Fatherland Front Committee of Hai Duong province, the representative of the Board of Directors of An Phat Holdings (APH) directly handed over VND 10 billion (~$425,000) in cash to the representatives of Hai Duong province to join hands and support Covid-19 prevention efforts in the province.

Earlier, at the beginning of February 2021, when Hai Duong detected many Covid-19-SARS-CoV-2 cases, An Phat Holdings donated 100 televisions and 40 tons of essential goods worth VND 1.35 billion (~$57,000) to the Committee for Covid-19 Prevention in Hai Duong province. With 2 times of support worth VND 11.35 billion (~$482,000), An Phat Holdings hopes to make a great contribution to join hands with the government and people of Hai Duong province to fight against Covid-19.

At the headquarters of the Vietnam Fatherland Front Committee of Hai Duong province, the representative of the Board of Directors of An Phat Holdings, Mr. Pham Van Tuan – Acting Deputy CEO of the Group directly handed over VND 10 billion (~$425,000) to the representative of Hai Duong. Hai Duong Province’s Leaders received donation from An Phat Holdings and expressed appreciation to the Board of Directors and employees of the Group.

Hai Duong Province’s Leader received VND 10 billion (~$425,000) support from representative of An Phat Holdings, Mr. Pham Van Tuan – Acting Deputy CEO (3rd from the right)Hai Duong Province’s Leader expressed appreciation for the support of An Phat Holdings

According to current situation, Hai Duong has become an epicenter of the country with 5 major outbreaks areas: Hai Duong City, Chi Linh, Cam Giang, Kinh Mon and Nam Sach. As one of the largest enterprises in Hai Duong, An Phat Holdings quickly call member companies to support Hai Duong to fight the epidemic.

On behalf of An Phat Holdings, Mr. Pham Van Tuan – Acting Deputy CEO shared: “We hope that the support from An Phat Holdings will be timely and able to help the Hai Duong government quickly respond, successfully controlled and stamp out the Covid-19. With the responsibility of an enterprise, we are willing to contribute human and material resources to help Hai Duong overcome this difficult period”.

Along with the community support, An Phat Holdings is actively coordinating with the local authorities to strictly implement prevention measures, ensuring safety for workers returning to work, maintaining production and business activities of the Group during the first quarter of 2021. Up to now, APH and 15 member companies have not appeared positive cases, An Phat Holdings is still absolutely safe.

Previously, in early 2020, An Phat Holdings also donated compostable products to 300 residents and soldiers on quarantine duty in Truc Bach area (Hanoi) and donated 5,000 medical masks and hand sanitizers to Vietnam Embassy in the United States.

At the end of October, nearly 5,000 employees of An Phat Holdings (APH) actively participated in support activities towards flooded people in Trieu Trung commune, Trieu Phong district, Quang Tri province. APH donated 3 tons of goods including rice, instant noodles, instant porridge, seeds, other essentials things to thousands of households in Trieu Trung commune.

September 27, 2020 marked an important milestone for An Phat Holdings, the 18th anniversary of the Group’s establishment. An eighteen – year journey is long enough for a plastic Group to assert its position well over the market as well as for An Phat Holdings (APH) to lay solid foundation to achieve great goals in the next stage – becoming a leading Group in high-tech and environmentally friendly plastics in Southeast Asia.

From a small business equipped with few machines and nearly a dozen employees, overcoming all hardships, with our diligence, enthusiasm and determination, An Phat Holdings (early known as An Phat BioPlastics JSC) has now been standing firm, strong and gained lots of successes. APH has been making great strides from a small packaging factory towards the No. 1 mono-layer packaging manufacturer in Southeast Asia.

Over 18 years of development, APH has built up a synchronous and comprehensive ecosystem in plastic industry, which consists of 15 member companies operating in different areas including: mono-layer packaging; biodegradable products; raw materials and chemical additives for the plastic industry; high-tech interior plastic products, engineering plastics, molding and precision engineering, industrial real estate, logistics services and trading.

The year 2020 marks an great milestone for the Group not only by accomplishments of business strategies, but also by good news: listing on the Ho Chi Minh Stock Exchange (ticker: APH) and increasing the total the number of listed member companies to four. Especially, after over 2 months of listing, with market capitalization VND 9,900 billion (~ USD 421 million), An Phat Holdings has became the largest plastic listed company in Vietnam.

In addition, the year 2020 also witnessed remarkable achievements of member companies. An Phat Bioplastics JSC (AAA) and An Tien Industries JSC (HII), respectively, awarded “Top 50 efficient companies”, “FAST 500” and “Prestigious exporter”. In particular, the most impressive accomplishment in 2020 is the launch of the project to build the biodegradable factory AnBio in Hai Phong for self-supply of raw materials and production of biodegradable products. The factory is designed with a capacity of 20,000 tons per annum, expecting to be constructed in 2021 and come into operation in 2022.

Despite the Covid-19 epidemic posing great challenges, APH’s member companies have not only fulfilled the 2020 business plan but also made encouraging progresses including expanding export markets of bioproducts from 5 countries in 2019 to 20 countries in 2020, An Phat Complex awarded the Top 10 most profitable industrial real estate company in Vietnam and engineering plastics members acquiring big domestic and international customers in supporting industry, etc…

In the supporting industry, APH is currently a reliable partner of many multinational corporations such as Honda, Toyota, Samsung, Piaggio, LG Electronics … APH is continuing to strive to become a 1st vendor for giant groups in the near future.

In particular, taking chance of production shifting to Vietnam, APH also boosts investment in the industrial real estate sector. In addition to An Phat Complex, APH invests in 180ha- Quoc Tuan An Binh as a new Industrial Park. The Group expected to clear the site by the end of 2020 and will go into commercial operation in 2021.