In China, PE prices have been steadily rising since the second half of June, with LDPE taking the lion’s share of these gains. As for PP, meanwhile, a stable to slightly firmer trend has dominated the market within the same period.

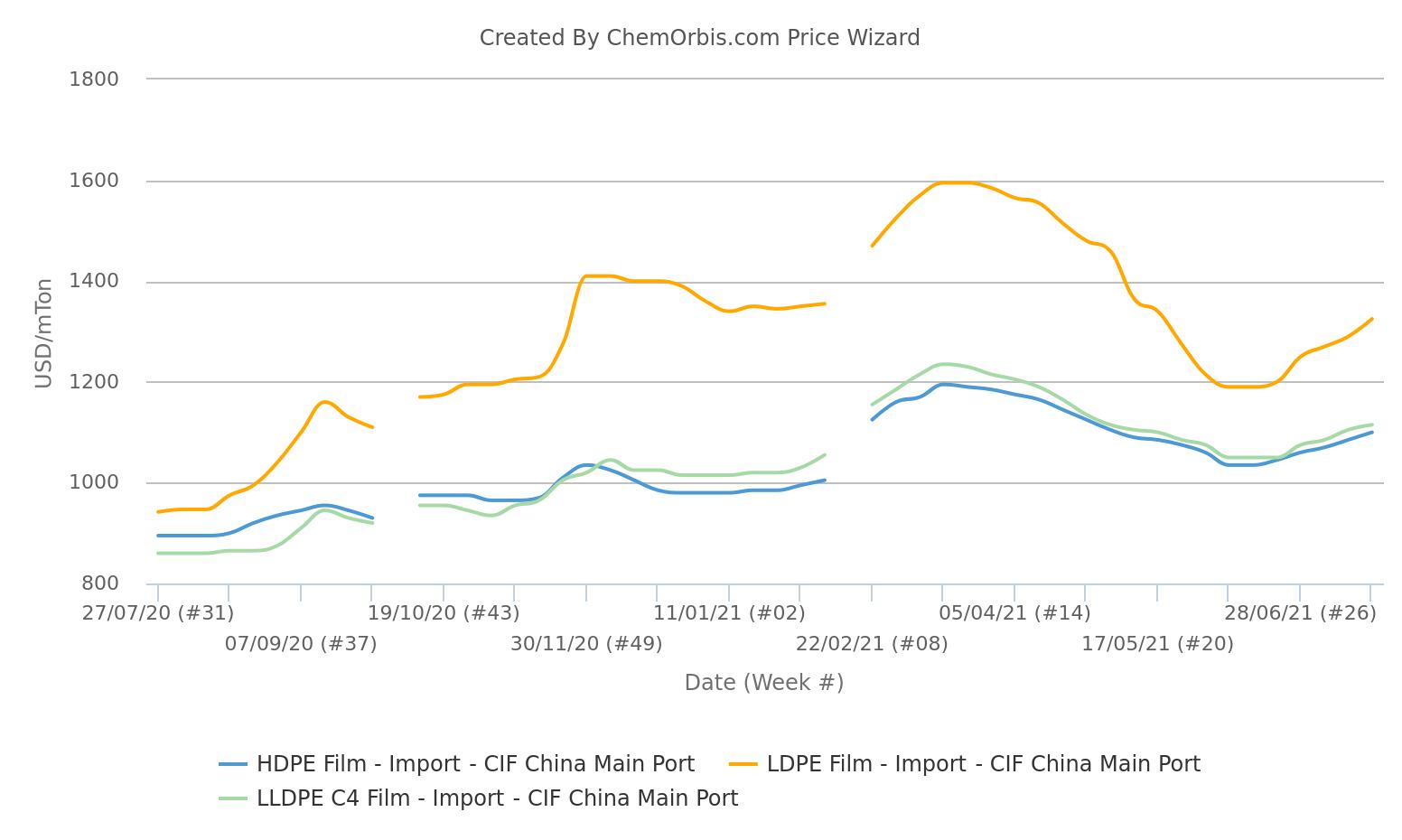

Import LDPE film prices rise to 2-month high

Supply tightness for import LDPE film has carried prices to the highest level since mid-May, ChemOrbis Price Wizard shows.

According to the weekly average data obtained from ChemOrbis Price Index, CIF China basis LDPE film prices have gained a total of $135/ton in the last five weeks to reach $1325/ton while LLDPE and HDPE film prices with similar terms have witnessed $65/ton increases during the same period to $1115/ton and $1100/ton, respectively.

“Import PE offers in China have been firmer, particularly for LDPE amid tight availability from the overseas markets. Local supply has also remained limited due to ongoing plant maintenance turnarounds at home. Despite some lingering demand concerns, domestic inventories have been drawn down sharply this week, reflecting higher consumption.

Dalian LLDPE futures have also rallied despite volatile crude oil prices and continued to support prices,” said a trader.

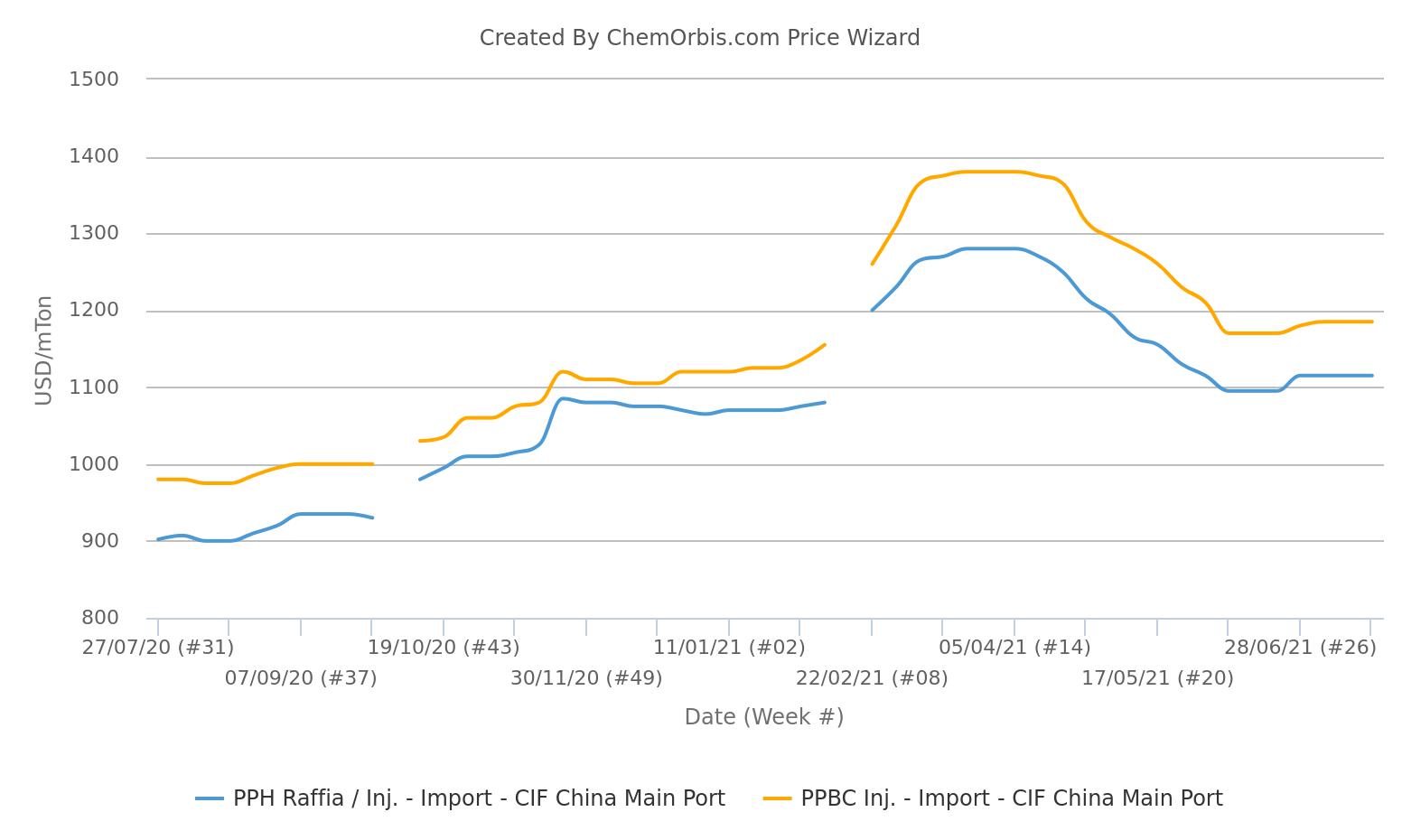

PP sentiment supported by low supply

ChemOrbis data also show that the weekly averages of homo-PP raffia and injection and PPBC injection offers are now standing at $1115/ton and $1185/ton CIF China, cash, respectively. If a slight firming in late June is disregarded, they have been mostly flat in the past five weeks.

“Import PP prices are flat due to limited availability from the overseas markets while there is also support from rising Dalian futures amid lower local inventories. Whilst the overall demand has remained limited with the lull season, there has been an uptick seen in buying activity this week, which has helped sentiment,” said another trader.

PP, LLDPE futures rise as demand pick-up seen

As of July 22, September LLDPE and PP futures on the Dalian Commodity Exchange posted weekly gains of CNY220/ton ($34/ton) and CNY283/ton ($44/ton), respectively. Firmer Dalian futures have pushed spot local PP and PE prices in China as well.

Despite volatility in energy values, Dalian futures have been driven higher by lower inventory levels inside China, reflecting demand pick-ups.

According to market sources, two major Chinese producers’ overall polyolefin stocks were reported to have declined by 45,000 tons on the week to 660,000 tons on July 22.

On a side note, concerns for the new capacities in China remain despite current low inventory levels. Around 1.3 million tons/year of LLDPE, 1.4 million tons/year of HDPE, and 1.9 million tons/year of PP are expected to become operational in the country in the July-August period.

Soure: chemorbis.com